By Bryan Gildenberg

Global strategy has for decades loosely segmented the world into “developed” and “emerging” markets, and growth strategy in the 21st century has often been a story of maximizing profits from developed markets to fuel growth in emerging ones.

Today most global companies have realized the limitations of this approach, as the U.S. remains a market that grows much faster than other “high income/capita” markets (a better phrase than “developed”). However, many of the practices and strategies being used to drive growth are either home grown or are being transferred from other rich countries.

In this piece, Retail Cities looks to help you understand the critical ways in which a more “emerging market” growth mindset can help unlock growth in the U.S. market.

Demographics

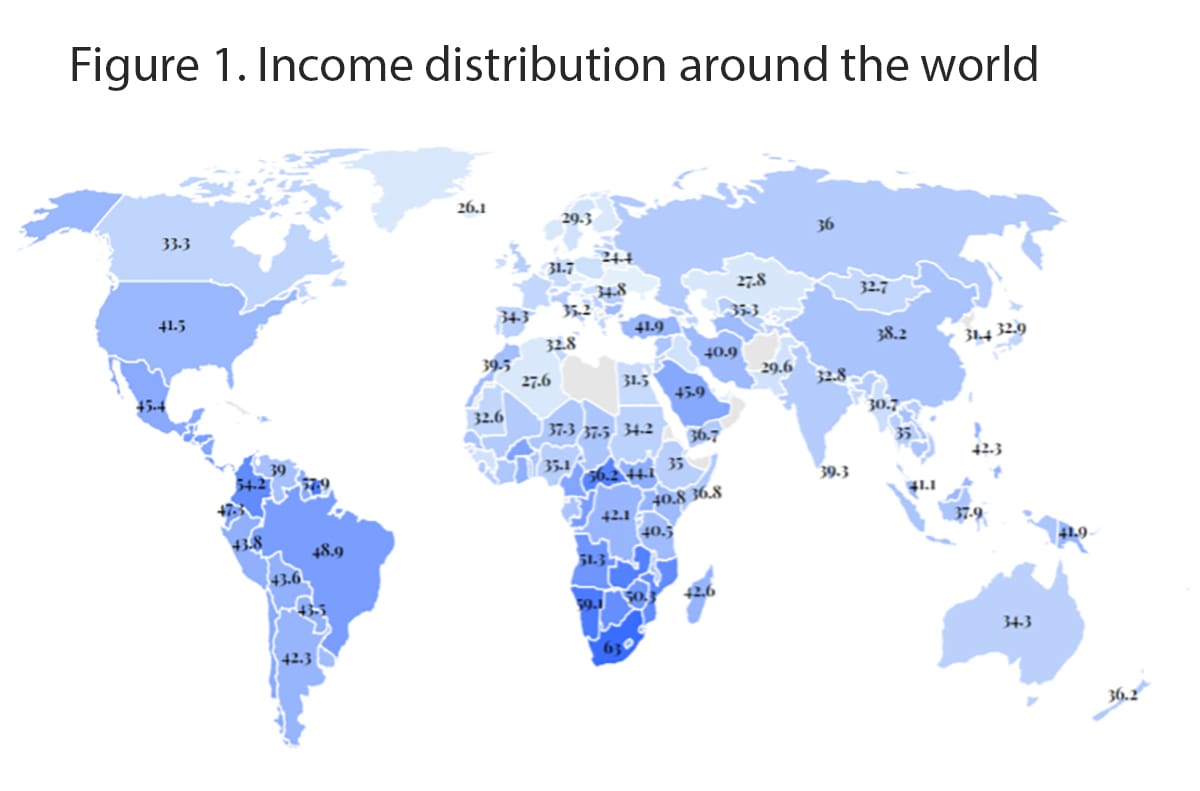

The most obvious place the U.S. has an “emerging” market profile is in income distribution. The best measure of income distribution is a GINI coefficient — the raw numbers don’t mean much, but the higher it is the less equal income is distributed. Looking at Figure 1, you can see that the U.S.’s peer group of countries in the equality game are markets like Brazil, Saudia Arabia and Turkey, not Europe, Australia or Canada.

Obvious Manifestation: Notably the rapid growth for decades of retailers like Costco and Dollar General that serve the high- and low-income markets.

Winning to 2030: Income data for commercial and media planning needs to be strongly calibrated for geography and cost of living — relative affluence is a better metric than salary.

Implication: In markets like Turkey, income distribution is hardwired into revenue growth management and price/pack architecture design principles in a way that is still a bolt-on or afterthought here for most brands. Retailers that serve both ends need markedly more differentiated format, merchandising and store operations approaches embedded into their core operating principles.

Other emerging market demographic points, highspotted:

• Age — The U.S. has a markedly younger demographic than most high-income-per-capita markets in the world — our age pyramid most closely resembles China’s of any major economy with a median age of 38 years old (here we’re joined by Australia and New Zealand that also skew younger than Canada or the major markets of Europe).

Key implication: Marketing platforms like TikTok that might be curiosities in other parts of the world are critical in a market that’s demonstrably younger than most other high-income countries.

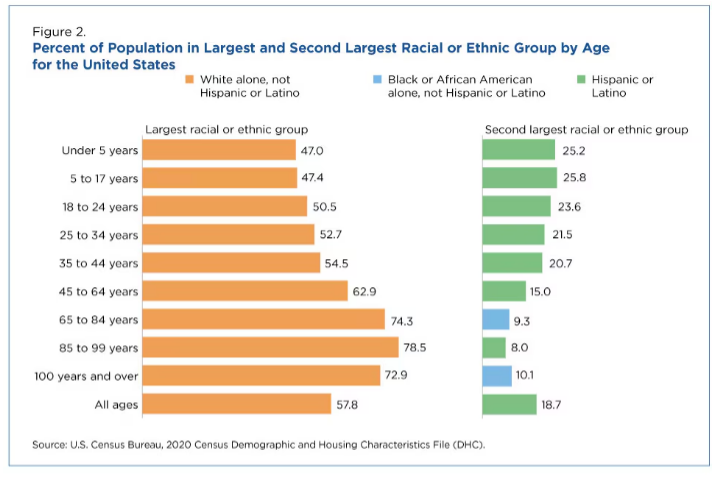

• Ethnic makeup + Age — Everyone knows the U.S. is ethnically diverse, but the intensity of that is particularly felt when we cross this diversity by age, as Figure 2 reveals. For under 35 America, the U.S. is a 50/50 caucasian/non-caucasian split — for Americans over 55 that split is closer to 75/25. The market with the dynamic that most closely reflects this is Brazil, whose 45+ population identifies as “white” and under 45 does not.

Key Implication: Speaking to consumers under 35 requires embracing a 50/50 world — without the right language, tone and approach brands/retailers aren’t just alienating the “minority,” they are alienating everyone who is growing up in an ethnically diverse world.

Health Care

Famously, the U.S. is the last high gdp/capita country in the world without universal health care. A list of the largest economies in the world that join the U.S. in this include China, Nigeria, South Africa and Pakistan. This creates a variety of issues for the U.S. that go well beyond the scope of this piece. Here, the focus is on the stresses this causes in the American health care system and how retail can help close the gap.

Obvious Manifestation: primary care gap — Depending on the source data, about 30% of Americans lack a consistent primary care provider. Retailers through in-store clinics and adjacent clinics are trying to play a more active role in primary care.

This has proven complicated, as 2024 has seen both Walmart (through closing its Health centers and Virtual Care unit) and Walgreens (exiting several markets with VillageMD) retrench their aspirations as alternative care providers. The challenge remains that in tackling anything related to the insurance/provider industrial complex, scale or a large fortune (like Marc Cuban’s) is necessary to really have an impact.

Winning to 2030: Primary care disintermediation — Retailers will be able to show the undercared a pathway to the connection between living healthy and saving money — through platforms like food as medicine, holistic well-being and affordable healthy living.

Implication: Retailers and brands will need to position themselves as a way to create health and wellness outside of the health care ecosystem. Too often health is sold as a premium solution to shoppers that are well served by health care — winning strategies with an “emerging market” mindset will unpack health care for people for whom retail and their phone are their most consistent health care touchpoints.

Other emerging market health care points, highspotted:

• Age — The U.S. has a markedly younger demographic than most high-income-per-capita markets in the world — our age pyramid most closely resembles China’s of any major economy with a median age of 38 years old (here we’re joined by Australia and New Zealand that also skew younger than Canada or the major markets of Europe).

Key implication: Marketing platforms like TikTok that might be curiosities in other parts of the world are critical in a market that’s demonstrably younger than most other high-income countries.

• Ethnic makeup + Age — Everyone knows the U.S. is ethnically diverse, but the intensity of that is particularly felt when we cross this diversity by age, as Figure 2 reveals. For under 35 America, the U.S. is a 50/50 caucasian/non-caucasian split — for Americans over 55 that split is closer to 75/25. The market with the dynamic that most closely reflects this is Brazil, whose 45+ population identifies as “white” and under 45 does not.

• Obesity — According to the Global Obesity Observatory (GOO) the U.S. is the ninth-most-obese nation on earth, joining a host of Pacific Island nations like Samoa; Qatar; Kuwait; and Romania in the global top 15.

Key Implication: The rise of GLP-1s and their next-generation cousins will continue to reshape the national conversation about weight management, but every business will need to transform as America either harnesses obesity or continues to creak under the cost of obesity-related ailments.

• Elder Care — A side effect of the health care system above is a responsibility for elder care to fall on patients and their families. The OECD states the U.S. spends less than half as a percentage of GDP what other high income/capita countries in the world spend here.

Key Implication: For most retailers and brands their primary role is in supporting the carer, not the caree — understanding the energy, time and emotional needs of families managing raising children and elderly parents is a critical growth platform.

Commerce

In many ways the U.S. retail marketplace is unusual for a high-income-per-capita country — most notably in its fragmentation. Fragmentation in terms of the number of retailers that make up 50%, 70% or 80% of retail (in many markets that number is less than five, whereas in the U.S. it is closer to 15). But the other critical piece is the level of business model differentiation — the top seven retailers in the U.S. have seven dramatically different business models — Walmart, Amazon, Costco, Kroger, Home Depot, Target and CVS.

The market this most closely resembles here is Turkey — another market with discounters, supermarkets, multi-format grocers and health and wellness stores competing for scale.

Obvious Manifestation: The U.S. requires an approach that can manage a wide range of channels through pack/price architecture, financial objectives and supply chain variance.

Winning to 2030: Channel/shopper matrixing — modular customer management. As each retailer develops its own complexity through both omnichannel and more diverse approaches to its store base for brands, each major customer may need to be managed to some degree the way the total market is managed now.

Other emerging market commerce points, highspotted:

• Urban versus Suburban

Key Implication: Understanding the cultural, route to market and e-commerce versus brick-and-mortar balance will be critical to winning the urban U.S.

• E-commerce pureplay-centric — In most high-income-per-capita countries e-commerce grew up omnichannel, whereas in the U.S., China and Latin America pureplay e-commerce retailers dominate digital commerce.

Key Implication: Global learnings for retailers and brands for the U.S. may learn more from the Brazilian shopper’s relationship to Mercado Libre than a European shopper’s connection to Amazon.

Conclusion

At Retail Cities we highlight the right ways to understand the global market to help grow your global business — stay tuned to us for more in-depth understanding of the ways an “emerging market” mindset can unpack U.S. growth.

Bryan Gildenberg is founder and chief executive officer of Confluencer Commerce.