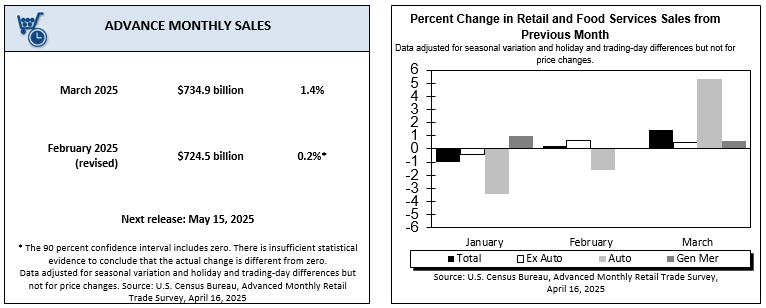

WASHINGTON – U.S. retailers saw a welcome boost in March as retail and food services sales climbed 1.4% over February to a seasonally adjusted $734.9 billion, according to new advance estimates released by the U.S. Census Bureau. The gain marks the strongest monthly rise in 2025 and reflects resilient consumer demand across key categories.

Year-over-year, March sales were up 4.6%, indicating continued momentum despite persistent inflationary pressures and cautious consumer sentiment earlier in the quarter.

📈 Headline Figures:

- March 2025 sales: $734.9 billion

- Month-over-month change (Feb to Mar 2025): +1.4% (±0.5%)

- Year-over-year change (Mar 2024 to Mar 2025): +4.6% (±0.5%)

- Jan–Mar 2025 vs. Jan–Mar 2024 total sales: +4.1% (±0.5%)

Note: All figures are seasonally adjusted, but not adjusted for inflation (i.e., nominal values).

🛍️ Retail Trade Breakdown:

- Retail trade sales (excluding food services):

- Up 1.4% from February

- Up 4.6% from March 2024

- Motor vehicle and parts dealers:

- Up 8.8% from March 2024

- Nonstore retailers (e.g., e-commerce):

- Up 4.8% year-over-year

Big-ticket categories lead the charge

The most significant gains came from motor vehicle and parts dealers, with sales soaring 3.1% month-over-month and 8.8% compared to March 2024. Dealers across the country reported stronger-than-expected showroom traffic and a return of discretionary vehicle spending, aided by stabilizing interest rates and improved inventory levels. For large format auto retailers and national dealership chains, this is a key sign that pent-up demand is beginning to convert.

Nonstore retailers—a category encompassing e-commerce platforms and digital-first businesses—saw sales rise 2.7% from February and 4.8% over the previous year. Retail analysts point to sustained online demand, particularly for apparel, home goods, and niche DTC brands, as a sign that digital continues to be a cornerstone of retail growth.

Mixed performance across brick-and-mortar segments

Results were more mixed for traditional store-based sectors. General merchandise stores, including department stores and mass merchandisers, saw a 0.9% monthly increase, while building material and garden equipment stores posted a modest 0.7% gain—a slowdown from earlier pandemic-era home improvement highs.

Clothing and accessories retailers posted a 1.1% monthly bump, though analysts warn that margins remain tight due to promotional activity and soft foot traffic in malls. Furniture and home furnishings stores rose 1.5% in March, helped by spring refresh purchases, though year-over-year growth was just 1.2%.

Grocery and health-related retail remained steady but unspectacular: food and beverage stores rose just 0.1% from February, while health and personal care stores grew 0.4%.

Quarterly momentum building

With the March numbers now in, the first quarter of 2025 shows retail and food services sales up 4.1% compared to the same period last year. While inflation has moderated compared to 2022 and 2023, elevated prices still affect real purchasing power. Nonetheless, consumers appear more confident heading into the spring season.

Looking ahead

Retailers are now preparing for key seasonal periods, including Mother’s Day and back-to-school, while keeping a close eye on macroeconomic signals like interest rates, wage growth, and employment numbers.

The Census Bureau noted that March figures are based on early estimates and will be subject to revision in its final report, due April 25, 2025. Additionally, upcoming reports will reflect updates based on new industry classification standards, which could impact comparative trends across sectors.

The next monthly retail sales data, which will include preliminary insights into Q2 performance, is scheduled for release on May 15, 2025.

{kind=link}