By Brian Owens

Today’s retail pharmacy sector continues to adjust to commercial headwinds from new digital insurgents and continued AI disruption, with less established pharmacy players and more emerging disruptors vying for consumer attention and loyalty. Utilizing brand equity measurement tools like BAV’s (Brand Asset Valuator’s) proprietary PowerGrid, and my experience as a managing director at BAV Group and retail industry expert for over 20 years, I have identified some new opportunities and challenges for the pharmacy sector. BAV is the world’s largest brand equity study, and it provides category agnostic brand fundamentals and measurements for over 60,000 brands tracked over 30 years across culture, based on surveyed stakeholder perceptions of brand strength and stature. Brand Equity is defined by Four Pillars as the foundation of the BAV model. Healthy brands develop the pillars in a very specific order: Differentiation, Relevance, Esteem then Knowledge. The Four Pillars are combined to form two dimensions — Strength and Stature — to capture a snapshot of a brand’s position in culture.

PowerGrid reveals key

insights for pharmacy brands

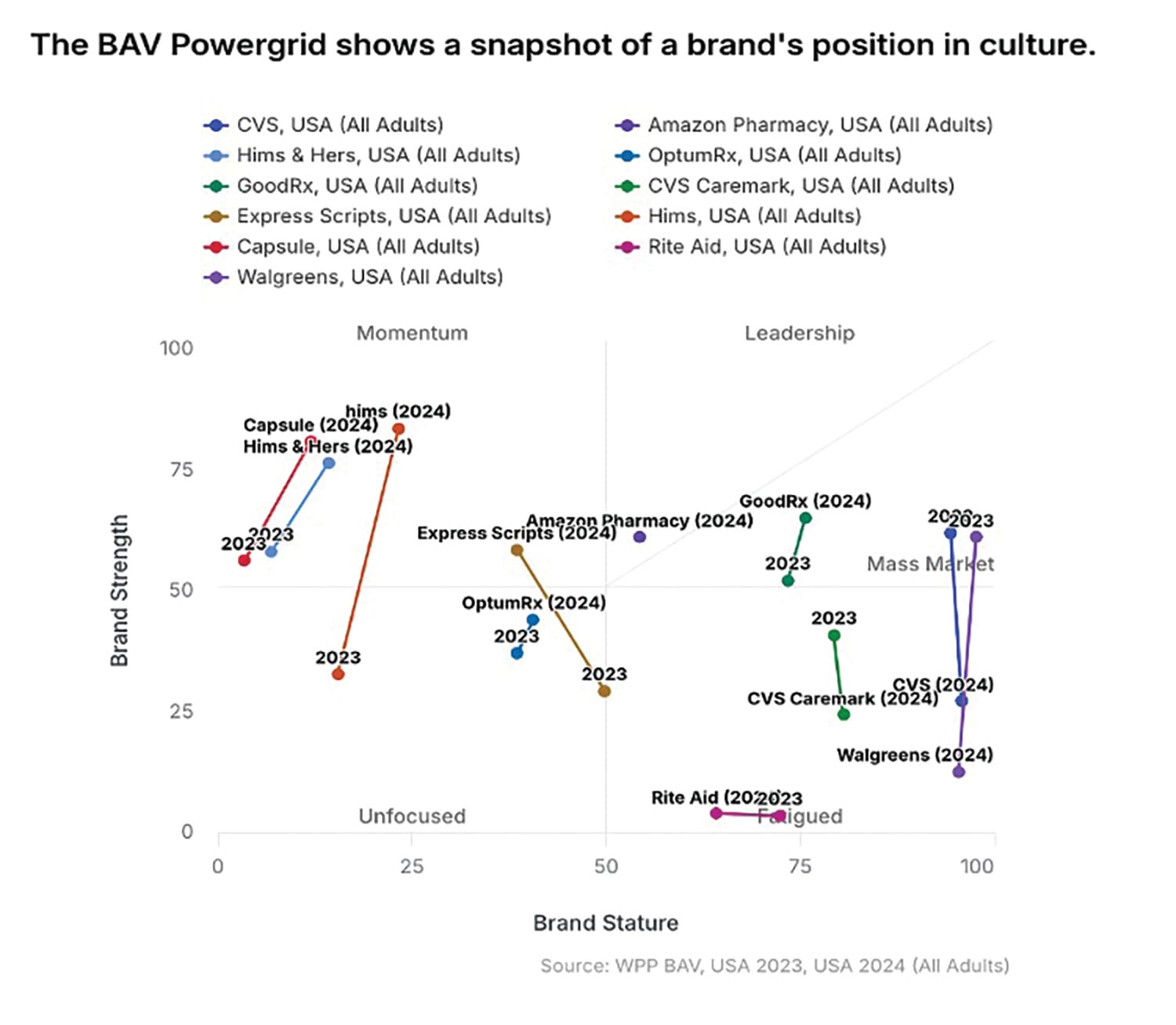

The BAV PowerGrid illustrates the brand strength and stature of a pharmacy’s brand. In the dataset, CVS and Walgreens rank highly for brand stature in both 2023 and 2024. However, their brand strength drops significantly in 2024 with CVS, Rite Aid and Walgreens all having the lowest brand strength ranks amongst pharmacy brands in 2024. This suggests that while these established pharmacy brands are well known and respected, they may not be seen as unique or innovative compared to other digital insurgent pharmacy competitors.

On the other hand, Hims & Hers and Capsule have high brand strength but relatively low brand stature. This indicates that these brands may offer unique products or services but are not as widely known or highly regarded as CVS or Walgreens. Interestingly, Hims & Hers has a significant increase in brand strength from 2023 to 2024 , showcasing their investment in brand campaigns. For example, their “Hands me, Not Hungover” 2023 campaign with NFL star Rob Gronkowski promoted their hangover defense supplement in a humorous, relatable way.

GoodRx and CVS Caremark maintain a balanced performance over the last two years. They have moderate to high scores in all categories, suggesting they are well regarded, known by consumers and offer some level of uniqueness in their offerings. GoodRx’s recent Stop Paying Too Much for Your Meds campaign highlighted their price comparison tools.

Trends shaping the pharmacy landscape

CVS and Walgreens, the two largest pharmacy chains in the United States, have been grappling with various challenges that have potentially impacted their brand strength. CVS has been facing increasing pressure on its PBM business due to heightened scrutiny over rising drug prices and the role of PBMs in the health care system. In 2023, the Federal Trade Commission launched an investigation into the practices of PBMs, including CVS Caremark, which could lead to further regulatory challenges and reputational damage.

Moreover, both CVS and Walgreens have experienced a decline in traffic as consumers continue to shift their shopping habits to other channels, such as online retailers and discount stores. The COVID-19 pandemic has accelerated this trend, with more people opting for e-commerce and contactless shopping options. As a result, the companies have been forced to adapt their strategies and invest in digital platforms to remain competitive.

The recent acquisition of Walgreens Boots Alliance by private equity firm Sycamore Partners presents significant challenges for Walgreens’ brand strength. The transition from being publicly traded to privately held may lead to changes in leadership, organizational structure and corporate culture, potentially impacting Walgreens’ ability to maintain a consistent brand identity and customer experience.

These multifaceted challenges emphasize the need for pharmacy brands to not only rely on their scale but also to differentiate themselves in a meaningful way and strengthen their connection with all consumers, not just the health-ready ones. By addressing these challenges head-on, pharmacy giants can work towards rebuilding their brand strength and securing their position in the highly competitive health care marketplace.

The nine elements of influence

The nine elements of influence are Innovation, Trust, Performance, Status, Purpose, Authenticity, Convenience, Fun and Contemporary (WPP BAV, 2024). These elements reflect different ways in which brands can be influential in culture. Each one, in isolation or in combination with others, can fuel brand growth and increase shareholder returns. Influential brands excel in at least one of these elements, creating a strong emotional connection with consumers that drives loyalty, advocacy and, ultimately, business success.

Strategies for CPG brands

CPG suppliers should be aware of several headwinds and tailwinds shaping this landscape. The Future 100 from VML highlights trends like the convergence of beauty and wellness, immersive retail experiences, and technology blurring physical and digital lines. Brands that align with these shifts, such as holistic self-care products, “awesperiential” pharmacy environments, and tech-infused health solutions, may find opportunities for growth.

To grow faster with pharmacies, consumer packaged goods brands should consider the following strategies:

• CVS and Walgreens: Collaborate on exclusive, innovative product lines and experiential activations that reinforce health authority while driving differentiation.

• Rite Aid and Capsule: Develop targeted assortments and content that appeal to older value-oriented and growing digital first Millennial and Gen Alpha audiences.

• Hims & Hers and GoodRx: Partner on co-branded lifestyle products and services that leverage their strong identities in the digital health space.

• Amazon Pharmacy: Offer seamless integration and compelling value that complements its convenience-driven platform.

To boost brand strength with pharmacies, CPG suppliers might find value in prioritizing:

• Prioritize Stores: Transform category spaces into destinations for wellness education, products and services that address fears, resentment and motivation.

• Convert Commerce: Use data to curate recommendations and experiences tailored to targeted audience needs, wants and goals.

• Create Attention: Develop exclusive brands with clear points of difference around ingredient quality, everyday lifetime benefits and public safety (sustainability).

• Connect Experiences: Blend physical and digital touchpoints in new ways that enhance access, convenience and multicultural growth audience access.

As the pharmacy landscape evolves, all brands must stay attuned to shifting consumer needs, and pharmacy suppliers that invest in differentiated offerings and create meaningful partnerships will be well positioned for success. By embracing the trends shaping the future of health and self-care, CPG suppliers and retail pharmacies can elevate public health, enrich consumers’ lives and grow more profitability.

Brian Owens is managing director of strategy and insights at BAV Group.

{kind=link}