By Todd Huseby, Tonny Huang and Michael Carr

The prescription drug value chain has followed predictable trends for the past several years: Pharma grows its capture of the profit pool, pharmacy benefit managers defend their share, and everyone else in the middle gets squeezed.

But we’ve now entered a pivotal moment in the industry’s history. New disruptions are shaking up the industry; now every player in the chain is feeling the combined effects.

Kearney has been advising clients on understanding the industry’s shifting trends and best positioning themselves for the future. For retail pharmacies, this year’s strategic planning exercise can and should look much different from recent years. This disruptive moment for the industry requires more nuanced and complex scenario planning, willingness to interface with new players and even new sectors, fresh thinking about partnerships and business models, and advanced sensing capabilities to stay on top of changes before they hit the bottom line.

In this article, we explore how the industry’s profit pools are changing, four future scenarios to consider, and how pharmacy leaders can get ahead of the turbulence to come.

Long-Steady Industry Trends Are Shifting

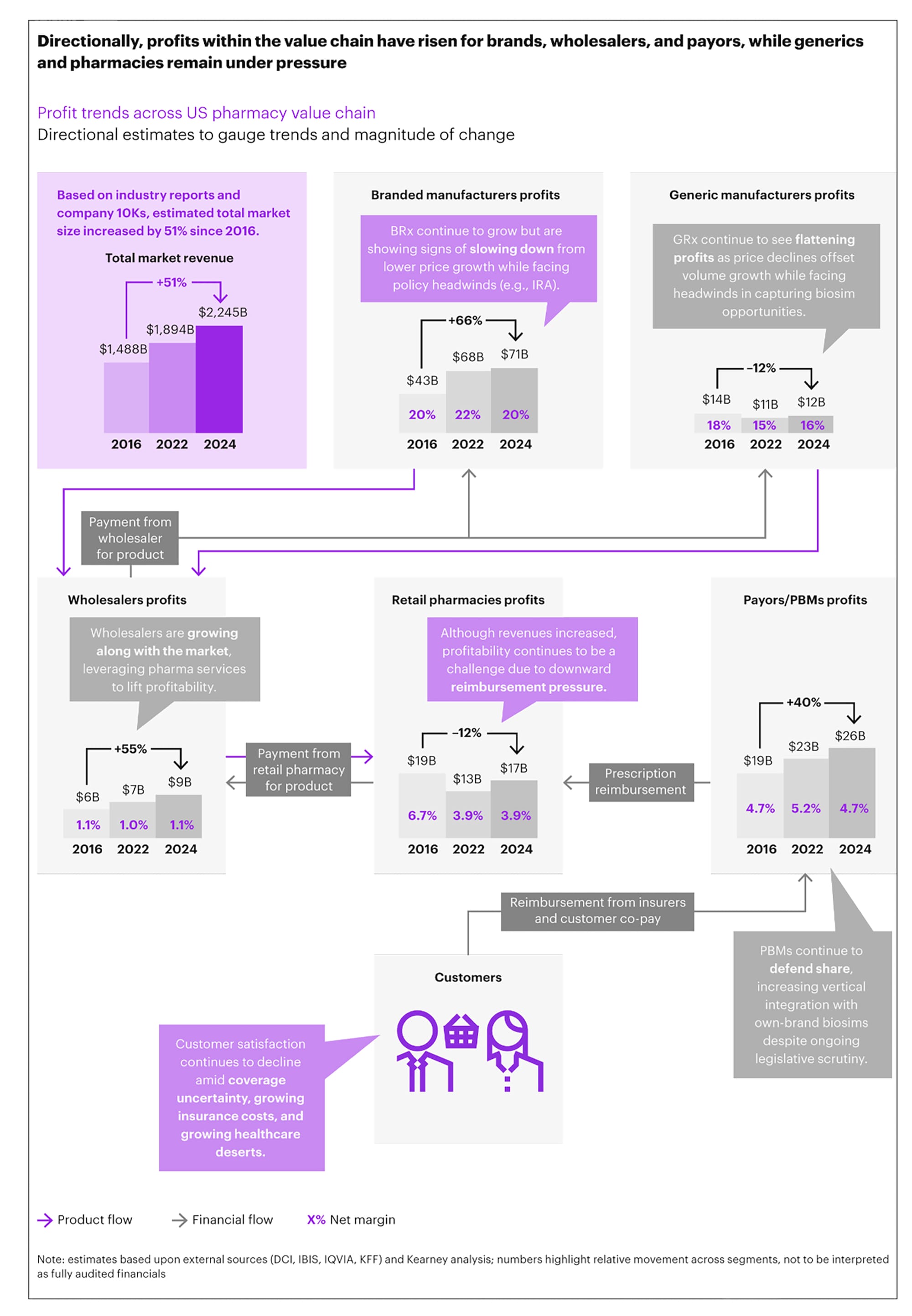

Every two years since 2016, Kearney’s consumer health practice has analyzed pharmaceutical profit pools to understand how the pharmaceutical value chain is faring financially. We ask: Who are the biggest winners and losers?

For years, our research has shown a continuation of long-running industry trends: Brand manufacturers kept capturing a larger share of profits, PBMs defended their share, and everyone in the middle (namely, retail pharmacies) was squeezed. But our latest research showed significant developments are disrupting that picture. Now, every player in the chain is feeling the effects of industry headwinds. Brand manufacturers, historically the most profitable part of the industry, are losing their share of profit.

Kearney’s research examines industry revenues and profits by segment, using estimates based on industry reports and public company financials. Our latest analysis shows that revenue in the pharmaceutical value chain has continued to grow, and is now more than 50% higher than the industry in 2016. However, profitability across segments has stagnated or declined compared to 2016.

Notably, in 2024, the breakdown of profit by segment broke with trends from previous years:

• Brand manufacturers: 53% of 2024 profit pool (-3% vs. 2022). Brand manufacturers’ profits grew at a significantly slower pace than the overall industry, driven by patent cliffs, policy headwinds and gross-net compression.

• Generic manufacturers: 9% of 2024 profit pool (+0.5% vs. 2022). Dispensing rates stabilized, but pricing remains deflationary.

• Wholesalers: 7% of 2024 profit pool (+1% vs. 2022). Thin margins persist. Wholesalers are increasingly diversifying into other health care revenue streams to boost profits.

• Retail pharmacies: 12% of 2024 profit pool (+1% vs. 2022). Profits are slim due to reimbursement mechanics, but retail pharmacies have hung on by focusing on operational efficiency, footprint rationalization and persistence of vaccinations in pharmacies long after the pandemic.

• Payors/PBMs: 19% of 2024 profit pool (+0.5% vs. 2022). The competitive landscape remains dominated by the big three players, despite mounting regulatory scrutiny and challenges from innovative PBMs with transparent pricing models.

For years, pharmacies have borne the brunt of industry pressures while profits have pooled with branded manufacturers. That makes sense in some respects: Branded manufacturers take the greatest risk and thus earn the greatest rewards, but increasing disruption from volatile U.S. health care policy, industry changes, innovative treatments and new fulfillment models are changing this picture; now everyone must be acutely adaptive to second-order impacts happening elsewhere in the value chain. It should trigger a broader conversation about the volatility ahead and the emerging scenarios that every player in the pharmaceutical space should prepare for.

Four Scenarios to Consider

Retail pharmacy leaders have a unique opportunity to proactively navigate the disruptions to shape the future of the industry. Pharmacies and pharmacists occupy a unique and trusted position helping individuals, families and communities access health care. They have hard-earned expertise, goodwill and respect that can be hard to translate to upstart and primarily digital channels. But pharmacies will need to reimagine themselves to keep that trust as the rest of the industry changes, and leaders will need to consider how to use pharmacy’s place in the health care ecosystem in navigating multiple future scenarios for the health care landscape:

• Public Policy Creates a Pricing Squeeze

One key driver of change affecting the industry right now: public policy action. Major legislation like the Inflation Reduction Act and the current administration’s Most Favored Nation pricing pressure are both aimed at lowering out-of-pocket costs for consumers and lowering government program expenditures.

While these policy pressures will primarily affect branded manufacturers, they will have a cascading effect throughout the industry. If branded manufacturers lose top-line revenue, they will more likely change their model to capture margin elsewhere in the value chain in the U.S. before they turn to other, smaller international markets.

• Patients Who Fall Off The “Coverage Cliff” Look for Alternatives

Under the One Big Beautiful Bill, public programs will have significantly reduced budgets, leading to reduced patient coverage. Insurance companies may withdraw from less profitable segments of their business, including public health plans.

As a result, more patients will be uncovered or undercovered. Some patients may have to look for alternatives to their current care plan; some may seek out over-the-counter alternatives, forgo treatment altogether or find non-pharmaceutical ways to support their health.

• PBMs Follow Industry Innovators to Make Drug Prices

More Transparent

In the past few years, there has been disruption in the PBM sector. One interesting example is Mark Cuban’s Cost Plus Drug Co., which transparently discloses the price structure for each drug, including its acquisition cost and a flat-rate consumer price. All of the “Big 3” PBMs have started to tout their own transparent models, but despite the fanfare, they seem more like point-of-sale rebates with low sponsor adoption and opaque GPO-related margins rather than a meaningful shift toward true transparency.

What could happen: As public scrutiny of PBMs continues, and more PBMs feel regulatory pressure, the incumbent PBM models could start to break down in favor of more transparent pricing models, following the lead of Cost Plus.

• GLP-1s Create a Broad Ripple Effect on Public Health and The Prescription Drug Market

Finally, as GLP-1s and other incretins continue to gain momentum in obesity, we may soon start seeing signals of impact in autoimmune, cancers, renal and other metabolic diseases. Realizing the fullest benefit for patients will require supporting physicians to enable earlier monitoring of cardio-renal-metabolic and other multi-organ health signals so they can administer combinations of both behavioral and pharmacological interventions at the right time. At a time when the popularity of GLP-1s is accelerating the maturation of the cash-pay, direct-to-consumer channel for prescription drugs to flow through, making sure the physicians can best guide patients through their care will be critical.

How Retail Pharmacies Can Adapt

For pharmacy leaders navigating this disruption, the annual strategic planning exercise is becoming increasingly complex. Retail pharmacies were already feeling the squeeze of slim margins; the new potential disruptions outlined above will add more uncertainty and change to the mix. Retail sits in a structurally weakened spot: The sector’s share of profits was flat but has been on a decade-long decline leading to this point, with competitive and disruptive pressures only further anticipated to increase in years to come.

At this point, reinvention is the only defense against steady margin erosion and diminished negotiating power. Elevated PBM transparency brought about with the passage of the 2026 Consolidated Appropriations Act will bring some reprieve to retail pharmacies in the form of greater visibility into steering patterns and strengthened “any willing pharmacy” contract standards, but pressures will likely persist, as history has shown PBMs to be highly adaptive in the face of dynamic policy environments and innovative competitors. Pharmacy leaders urgently need to question traditional models, revisit innovative partnerships that were deemed unfeasible before, and invest in capabilities to meet the moment, no matter what’s to come. Instead of hunkering down and staying siloed, leaders can bring fresh thinking and build new ways of collaborating and integrating across the industry, new ways of working internally and with patients, and new models for success.

Adjusting to moments of major change is difficult and uncomfortable. But here’s the end result: If pharmacy leaders succeed in navigating this period of uncertainty, they have the ability to reshape the drug value chain to deliver more affordable, quality medicine for patients. That’s a change that’s worth pursuing.

{kind=link}