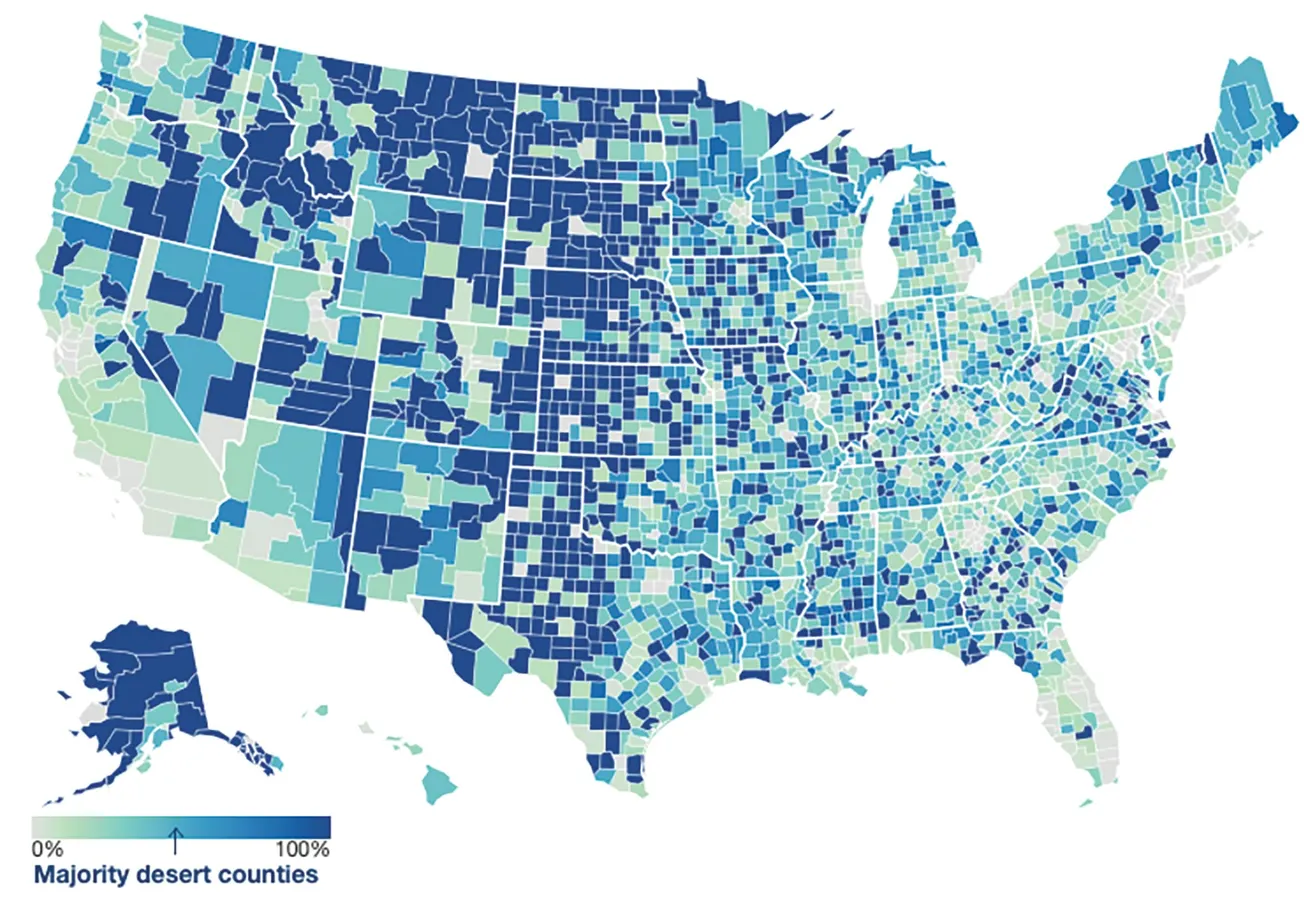

Figure 1. U.S. population living in a pharmacy desert

Major drug store chains in the U.S. — namely, CVS Health, Rite Aid and Walgreens Boots Alliance — opened stores at a rapid pace for many years, usually in street corner locations to provide the highest level of convenience to their customers. However, in the past two years, we have seen a reversal of this trend as these retailers pivot from endless expansion to closing hundreds of stores to cut costs and increase margins.

Deborah Weinswig

Many regions in the U.S. can already be characterized as “pharmacy deserts,” meaning they have poor access to prescription drugs. The growing number of drug store closures in the U.S. will exacerbate this issue, impacting the health and well-being of individuals, especially those who rely on regular prescriptions to manage chronic conditions.

Lost in the sands: The extent of the issue

There are a number of factors that contribute to poor pharmacy access, including low income, insurance status, high prices, inadequate mobility and long distances. The definition of a pharmacy desert varies by type of location and is dependent on a minimum distance (threshold) between the majority of residents and their closest drug store: 10 miles for rural locations, two miles in the suburbs, one mile in urban locations, and just half a mile in low-income urban or suburban neighborhoods where few households own cars.

Having convenient and adequate access to pharmacies is imperative, as nearly three in five Americans age 18 to 64 use at least one prescription drug (according to a June 2023 report by the National Center for Health Statistics) — a figure that is likely to rise as the U.S. population ages. Furthermore, older patients are more likely to experience difficulties accessing pharmacies due to age-related difficulties, and they may struggle to visit pharmacies that are located miles away from their homes due to transportation limitations.

According to a Public Health Post study in 2021, one in every three neighborhoods in 30 U.S. cities are pharmacy deserts, affecting about 15 million people. In the same year, health care company GoodRx reported that over 40% of all U.S. counties are considered pharmacy deserts. States such as Alaska, Idaho, Kansas, Montana, North Dakota, South Dakota and Texas contain many pharmacy desert locations, while cities including Albuquerque, Baltimore, Boston, Chicago, Dallas, Los Angeles, Milwaukee and Philadelphia have noticeable disparities in pharmacy accessibility, according to a 2021 study by the University of Southern California.

The desert heats up: Drug store downsizing

The issue of pharmacy deserts is becoming more prevalent as store closures have become common among major drug store chains as they reconfigure their operations to improve operating margins in response to increased competition from online players and nonspecialist retailers, evolving consumer buying patterns, and changes in the U.S. population. The majority of drug store sales come from filling prescriptions. However, profits from that segment have declined in recent years due to lower reimbursement rates for prescription drugs. The front end of drug stores, where they sell discretionary products, also faces weak demand due to consumers’ cautious spending habits in response to persistent inflationary concerns.

U.S. labor shortages have also contributed to store rationalization, which forced CVS Health and Walgreens to reduce pharmacy store hours in 2023 — and they faced labor strikes in October and November 2023 due to increased staff workloads amid labor shortages.

This trend also comes amid increased digitalization and a push into health care services by many major players in the space, both of which necessitate significant investments; store closures enable retailers to make cost savings.

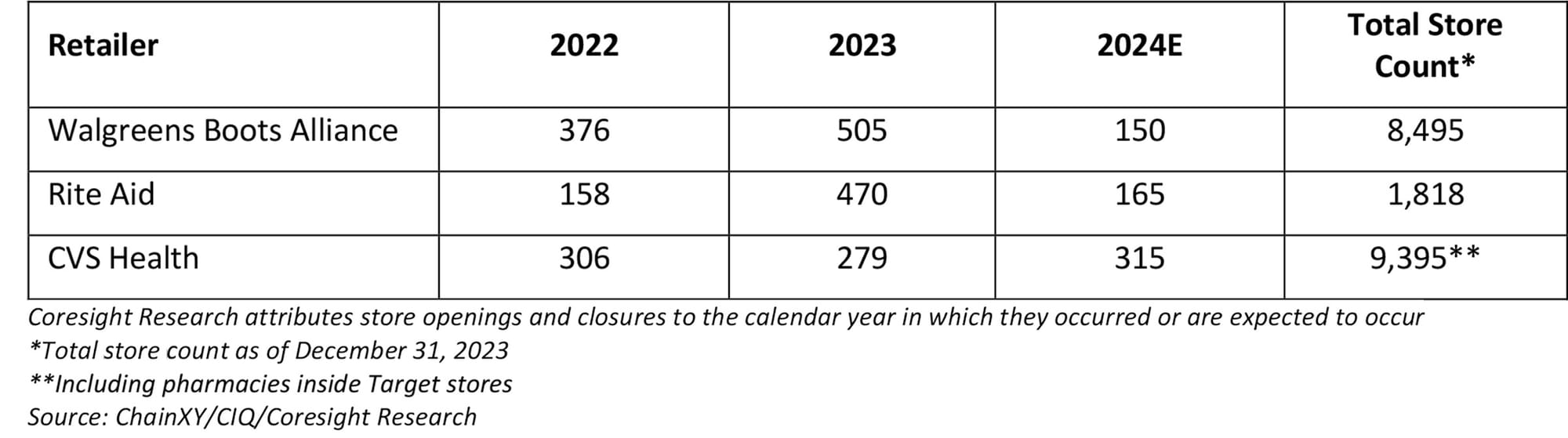

• In 2021, CVS stated that it would close 900 stores by the end of 2024, representing about 10% of its total fleet. The retailer stated in February 2024 that it has closed 630 of these so far and is on track to reach its target. CVS also announced in January 2024 that it will close some of its pharmacies operating in Target stores by April 2024.

• Rite Aid has accrued large debts and experienced an increased cost burden due to opioid crisis-related compensation and has been restructuring its business through Chapter 11 bankruptcy protection (filed in October 2023) and liquidating its stores. The retailer has targeted the closure of 400 to 500 stores (no timeline given), which represents nearly one-quarter of its total footprint.

• In 2023, Walgreens announced that it would shut 150 stores in the U.S. in 2024. The retailer has already reduced store hours and cut corporate jobs in a first round of cuts aimed at reducing costs by $800 million by the end of 2024.

Finding an oasis: Retailers poised to gain advantage

Store closures in the drug store sector may ultimately result in a higher number of pharmacy deserts in certain parts of the U.S. This could benefit big-box retailers such as Walmart, as well as dollar store chains such as Dollar General and Dollar Tree, which have already entered the retail pharmacy space and have expansive store networks and a physical presence in rural areas. Around 75% of the U.S. population lives within five miles of a Dollar General store, and 90% live within 10 miles of a Walmart store, according to these retailers, representing unique access to rural communities that are often underserved by the current health care ecosystem in the U.S.

Furthermore, these retailers have plans to continue with their store network expansion plans, which would help fill the gap in pharmacy accessibility left by drug store closures:

• Dollar General plans to open 785 stores in the U.S. this fiscal year, ending early February 2025.

• Dollar Tree plans to open 650 stores in its current fiscal year, ending early February 2025.

• Walmart plans to open 150 stores in the U.S. in the next five years, from February 2024.

Telepharmacy or e-pharmacy can also play a vital role in catering to communities underserved by physical pharmacies. Tapping this opportunity, Amazon launched RxPass in January 2023, a new Prime membership benefit from Amazon Pharmacy that offers patients affordable access to commonly prescribed generic medications. RxPass allows Prime members to receive all qualifying prescriptions for a monthly fee of $5.00 (delivery included).

What we think

Pharmacy deserts present a number of issues for consumers, including longer travel times to receive drugs, fewer options for seeking health care advice and potential gaps in medication adherence. This issue is especially concerning for vulnerable groups (such as older people), low-income consumers and those living in rural areas.

A comprehensive strategy involving cooperation between legislators, health care providers and community stakeholders is needed to address the issue of pharmacy deserts and make certain everyone has fair access to required pharmacy services.

To mitigate the effects of drug store closures, policy makers should provide incentives for pharmacies to open in underserved areas and boost financing for community health centers.

Deborah Weinswig is founder and chief executive officer of Coresight Research.

{kind=link}